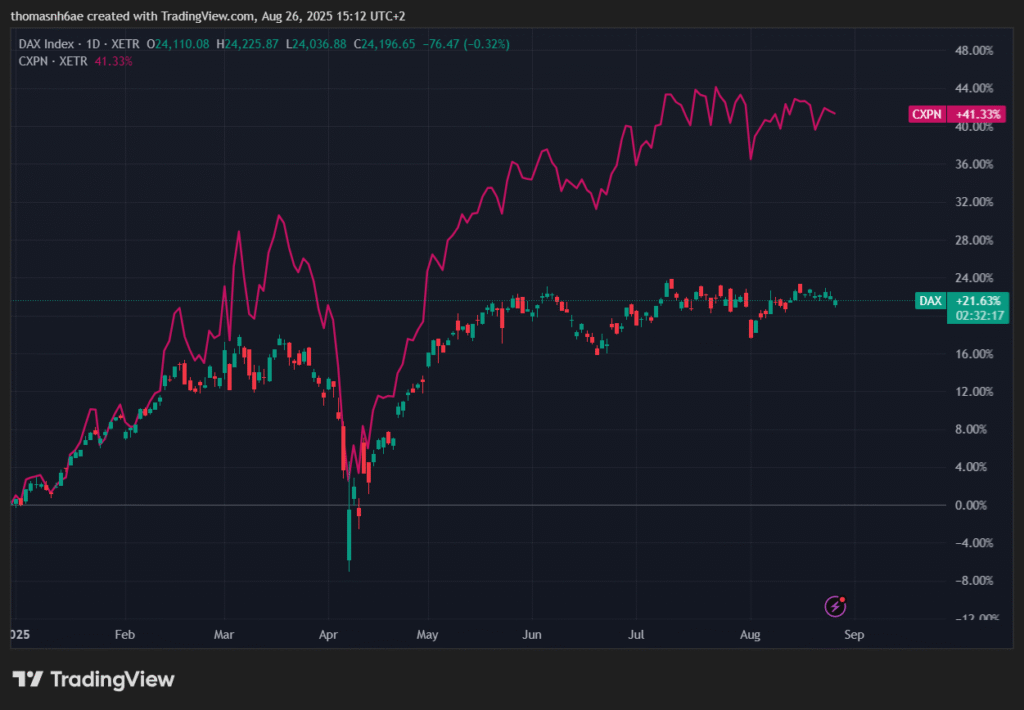

Der Kaiser Fiscal Stimulus

This fractal is focused on German fiscal stimulus package. Our analysis is framed by the findings of the Research Affiliates paper, “Stimulus Does Not Stimulate,” which posits that for fiscal stimulus to be effective, its positive effects must materialize within a 12-18 month timeframe. The paper further underscores that such measures are most successful during periods of recession, a condition that Germany has experienced over the past two years.

You can find the result of our analysis right below with the Der Kaiser Basket:

Key Fiscal Stimulus Details:

The German government has allocated a significant investment budget of €500 billion over 12 years, distributed as follows:

- €300 billion for infrastructure development.

- €100 billion for climate and ecological transition initiatives.

- €100 billion to support businesses receiving state subsidies, with a particular focus on small and medium-sized enterprises (SMEs) within the MDAX index.

Our analysis identifies specific companies poised to benefit from this stimulus, categorized by sector. This presentation is based on a chronological order.

For the stimulus to work, energy needs to be cheap and therefore imported in large quantities. When this energy flows into the economy, the materials sector and raw material providers should be impacted.

Finally, the industrial sector should benefit from all the advantages accumulated by the previous sectors, because the industrial sector is the directtarget of the stimulus. This sector will create jobs and relaunch the economy.

Our assessment highlights three core sectors—Energy, Materials, and Industrials—as the primary beneficiaries. These industries represent the foundation of Germany’s economic structure and are positioned to capture early gains from increased capital injection and infrastructure-related spending.

In addition, the Pharmaceuticals and Chemicals stocks stand to benefit, particularly from targeted tax incentives related to investment in new machinery and research & development. However, given the longer innovation and regulatory cycles in these industries, the positive impact is expected to materialize more gradually compared to the immediate uplift in the core industrial sectors.

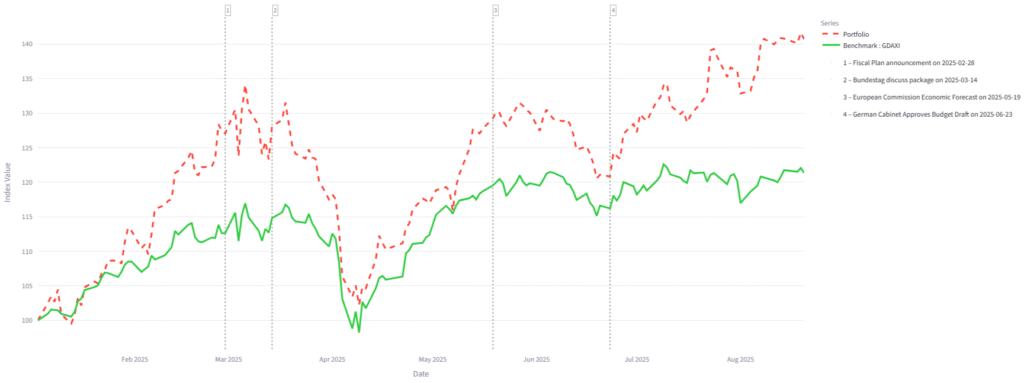

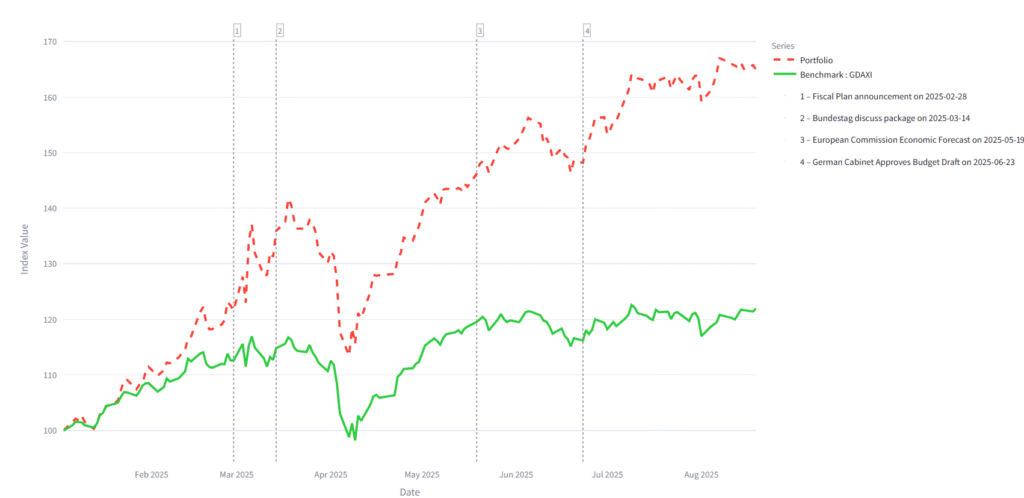

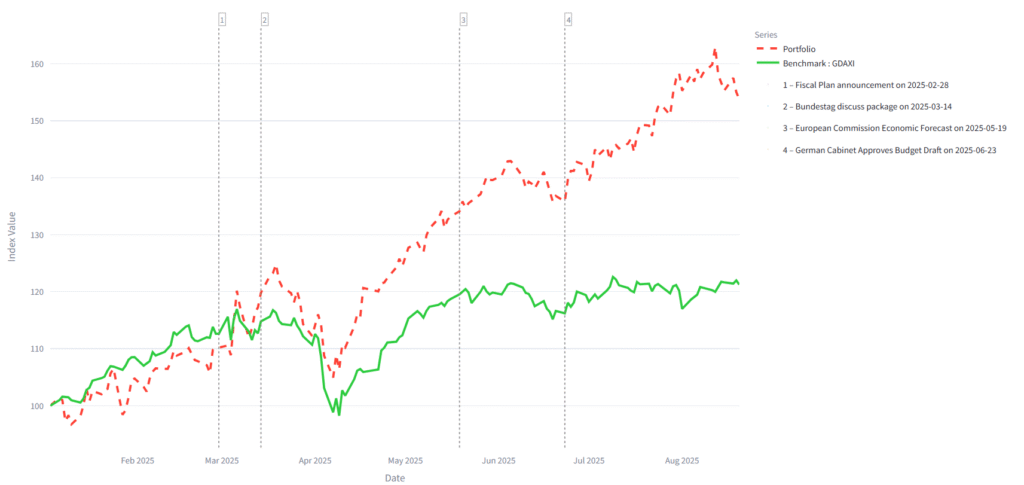

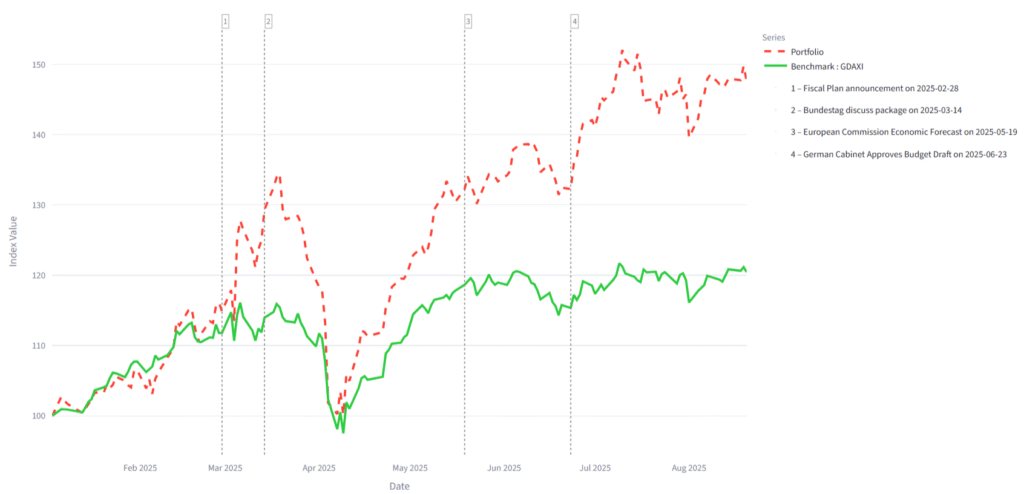

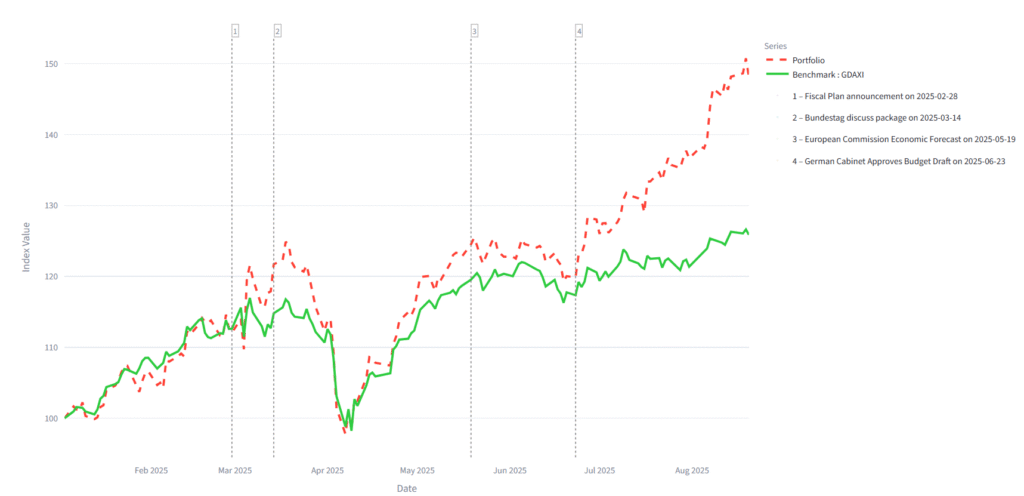

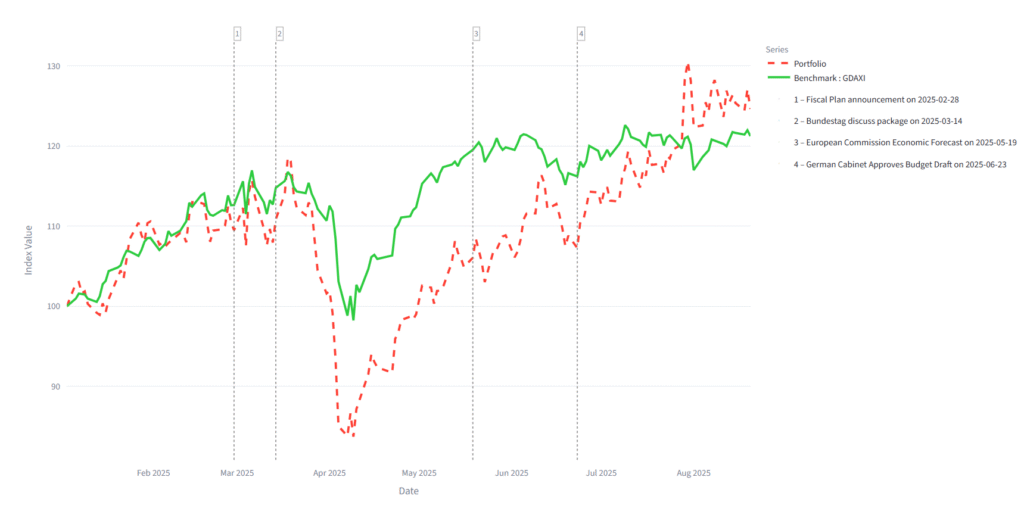

On this chart we already see a clear outperformance form the industries compare to the DAX: Graph start on 28 February.

Date Selection:

Fiscal Plan announcement

The date of February 28, 2025, was chosen for a significant event: a meeting at the White House between President Trump and President Zelensky, reports indicate that this visit ended abruptly. This incident has been described as a major shock, prompting Germany and other European countries to take a more assertive role in their own defense, recognizing that they cannot always rely on the United States for support. On Tuesday, German Chancellor F. Merz announced his 500-billion-euro fiscal plan.

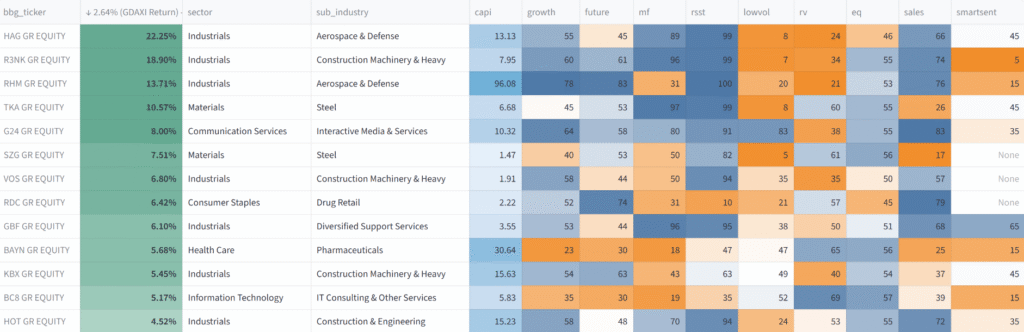

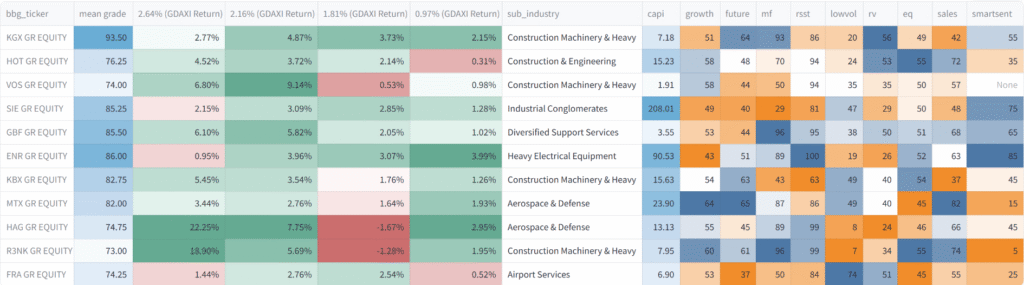

We observe a clear dominance in the defense sector, reflecting Europe’s ongoing rearmament efforts. Notably, Renk (R3NK) + 18.90 %, Rheinmetall (RHM) +13.71% is leading in munitions production, while Hensoldt (HAG) +22.25% specializes in radar sensors and other transmission technologies.

In parallel, the steel industry shows strong momentum, with Thyssenkrupp (TKA) + 10.57% and Salzgitter (SZG) +7.51% standing out. The pharmaceutical sector is also performing well, with Bayer (BAYN) + 5.68% delivering solid gains.

Across these segments, we see consistent outperformance relative to the broader market, underscoring investor confidence in industries tied to defense, industrial resilience, and healthcare innovation.

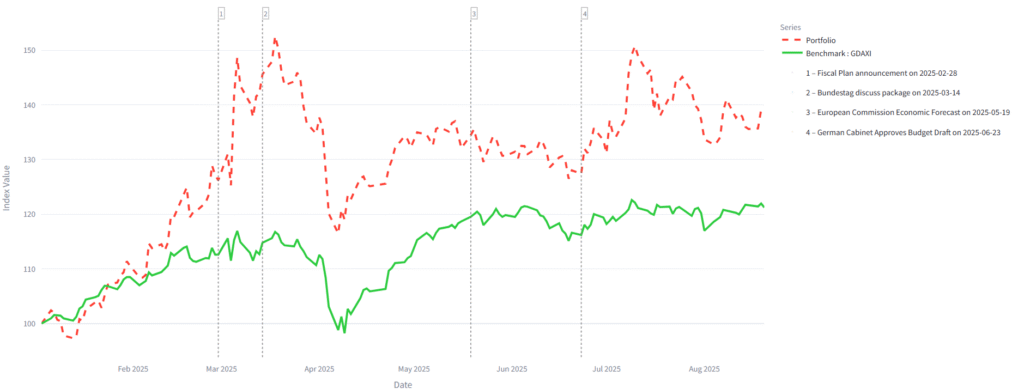

Bundestag Discuss Package

March 14, 2025, was significant because it marked the day the new German government, led by Chancellor Friedrich Merz, secured the support of the Greens for a crucial borrowing package that was to be voted on a few days later. This agreement was a major breakthrough in the post-election government formation process. ( Market already anticipated the move before the vote)

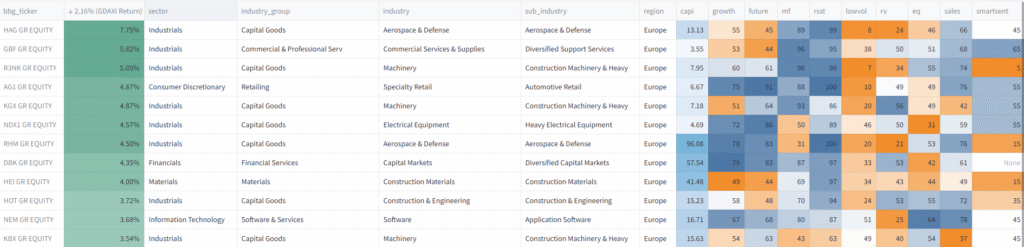

Compared to the previously selected date, we observe a shift in relative performance across sectors. Defense stocks continue to lead, with Hensoldt (HAG) +7.75%, Renk (R3NK) +5.69%, and Rheinmetall (RHM)+ 4.50% maintaining strong momentum. However, new beneficiaries are emerging, particularly Bilfinger (GBF)+5.82% and Nordex (NDX1) +4.57% , which are positioned to capitalize on the stimulus plan.

Green Industrial LeadersNordex (NDX1) stands out as a potential first mover, driven by its focus on efficiency and renewable energy through wind turbine technology. Companies that combine an industrial backbone with climate-conscious solutions are likely to be among the biggest winners of the plan.

Similarly, Heidelberg Materials (HEI) +4.00% is set to benefit from reconstruction demand, leveraging its green cement products, which command a premium price—up to three times higher than conventional materials. If supported by subsidies or reduced production costs, this could significantly boost earnings.

Supply Chain and LogisticsKION Group (KGX) + 4.87%, specializing in trucks and supply-chain solutions, is another early-stage beneficiary. As economic momentum builds, companies initially prioritize efficiency in distribution and logistics, which in turn lays the foundation for sustainable growth in production.

Enablers and Adjacent Sectors We also see potential in Nemetschek (NEM) +3.68%, which provides software solutions for infrastructure design and architecture, as well as Hochtief (HOT) specialised in construction (data centers, health care, educational facilities …) and energuy transition. These enablers are positioned to capture secondary benefits from infrastructure investment and construction activity.

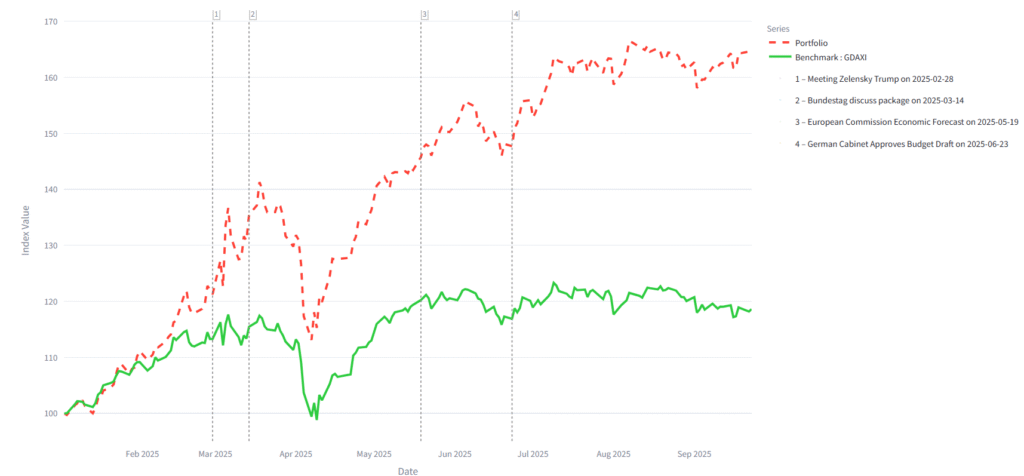

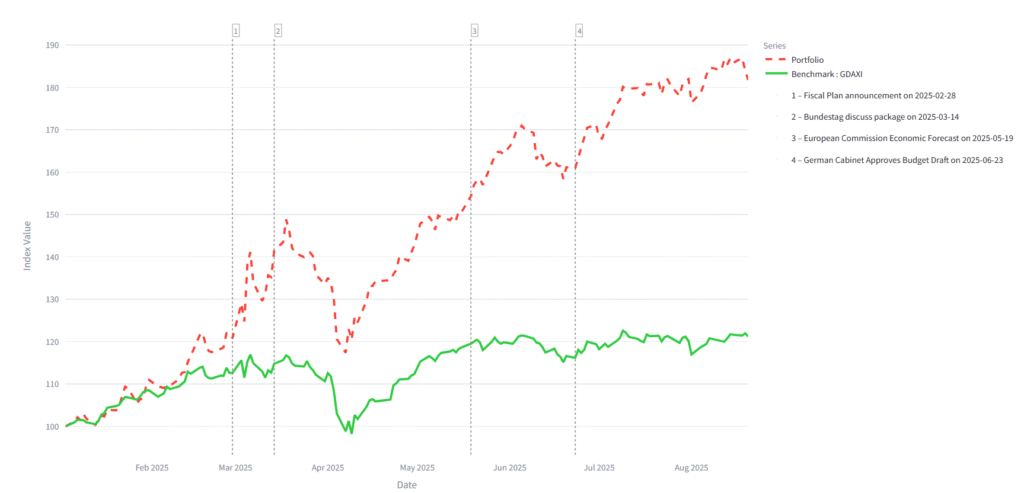

European Commission Economic Forecast

On May 19, 2025, the EU Spring 2025 Economic Forecast projected that eurozone inflation is falling faster than expected, putting it on course to reach the ECB’s 2% target this year and giving the central bank room to continue cutting interest rates. For Germany, this environment translates into households regaining purchasing power while cheaper financing supports its export-oriented industries. Together, these factors are set to benefit industrial players such as Siemens and Bilfinger, as well as green energy firms including Nordex and Siemens Energy.

Germany’s economy is forecast to grow by 1.1% in 2026, a sharp turnaround from the -0.2% recession in 2024, while EU-wide growth is projected to reach 2.1% in 2026. Click here for more details (1, 2)

Large-scale initiatives in areas such as cancer research continue to attract substantial funding. Companies like BioNTech (22UA) +4.70% and Dermapharm (DMP) +2.47%, as well as Redcare Pharmacy (RDC) +2.87%, are well positioned to benefit. Both specialize in large-scale distribution—one in oncology, the other in patent-free pharmaceutical products. In the near term, it is the major pharmaceutical players that stand to gain the most from this stimulus, given their established distribution networks and shorter time-to-market advantages in reaching broader customer bases.

The recent strength in Auto1 Group (AG1) +3.27% and Traton (8TRA) +3.09% highlights the resilience of Germany’s auto sector. While it may be premature to expect direct gains, the sector remain strategically important for the German economy. Although new EVs remain relatively expensive, the second-hand EV market is emerging as a key growth driver. This segment offers a more affordable entry point for consumers, enhances liquidity in the used car market, and provides an adoption that accelerates penetration across both B2B and B2C channels. With rising demand, improving charging infrastructure, and favorable regulatory support, the second-hand EV space stands out as a potential outperformer with above-market growth prospects.

Enablers also play a crucial role. For instance, Kion Group (KGX) +2.15% continues to provide exposure to logistics and supply chain automation, while Siemens Energy (ENR) +3.99%, the European leader in energy production, remains a champion in delivering low-cost energy across Germany and Europe. Both represent strategic pillars in supporting industrial competitiveness and energy transition across the region.

German Cabinet Approves Budget Draft

On 23 June 2025, the German Cabinet has approved the 2025 draft budget, featuring a record €115.7 billion in investment, set to rise above €120 billion in 2026, alongside a €500 billion special fund for infrastructure and climate neutrality (Reuters; DW). Defense spending will also rise sharply, from €95 billion in 2025 to €162 billion by 2029. This marks a historic break from fiscal restraint, with total borrowing of €847 billion planned through 2029. Markets reacted positively, with equities—particularly cyclicals, defense, and infrastructure stocks—firming in response.

The budget further provides increased funding for social housing construction and the social security system. However, financing these projects through large-scale government borrowing will increase the supply of German government bonds (Bunds), which typically exerts upward pressure on bond yields—a key benchmark for interest rates across Europe.

Masterial

Aurubis (NDA) +5.13% is well placed to benefit from the budget’s infrastructure and electrification focus. As Europe’s largest copper producer, it is directly leveraged to rising demand for grid expansion, EV charging networks, and renewable energy systems. Heidelberg Materials (HEI) +3.28%Heidelberg Materials stands to gain from the surge in public investment in construction and transport infrastructure. Cement and aggregates are essential to Germany’s modernization program, and the company’s emphasis on low-carbon solutions aligns with regulatory support for sustainable building.

Wacker Chemie (WCH) +3.19% is strategically exposed to clean-tech value chains. Demand for its polysilicon will grow with expanded solar capacity, while specialty chemicals are critical inputs for batteries and EVs. The climate-neutral agenda embedded in the budget enhances Wacker’s role in both energy and mobility transitions.

Industrials

Siemens (SIE) +2.85% is a clear winner from Germany’s fiscal pivot. The group’s businesses in electrification, automation, and digital infrastructure directly benefit from higher state investment in grids, transport, and industrial modernization. Siemens’ diversified portfolio positions it to capture growth across multiple verticals supported by the budget.

Daimler Truck (DTG) +2.78% gains from increased infrastructure and logistics activity, which translate into higher demand for heavy-duty vehicles. As supply chains expand and transport volumes grow, DTG stands to benefit both from cyclical tailwinds and from structural shifts such as the transition to zero-emission trucks. The stimulus plan reinforces the company’s role as a backbone of German and European industrial logistics.

Technology

Infineon (IFX) +3.89% stands to benefit from the budget’s emphasis on digitalization, electrification, and energy transition. As Europe’s leading semiconductor producer, its power electronics are critical for EVs, renewable energy integration, and industrial automation. With rising demand for chips in both mobility and clean energy, IFX is positioned as a strategic enabler of Germany’s investment cycle.

Baskets Der Kaiser Fractal

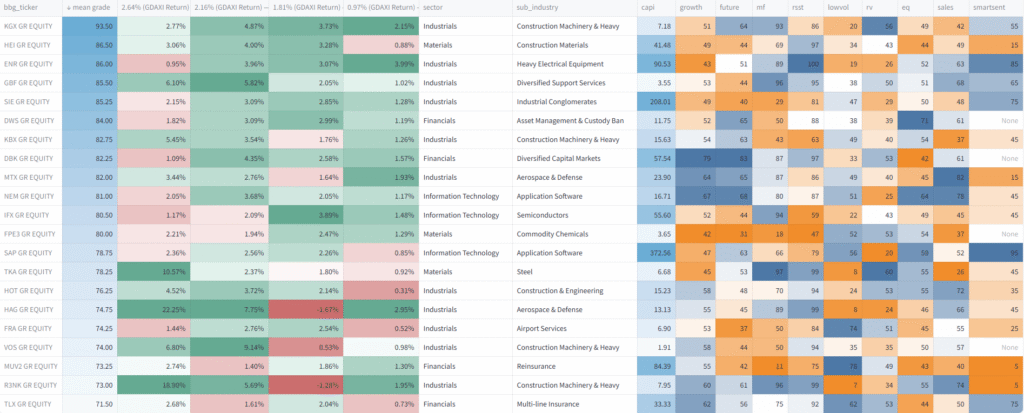

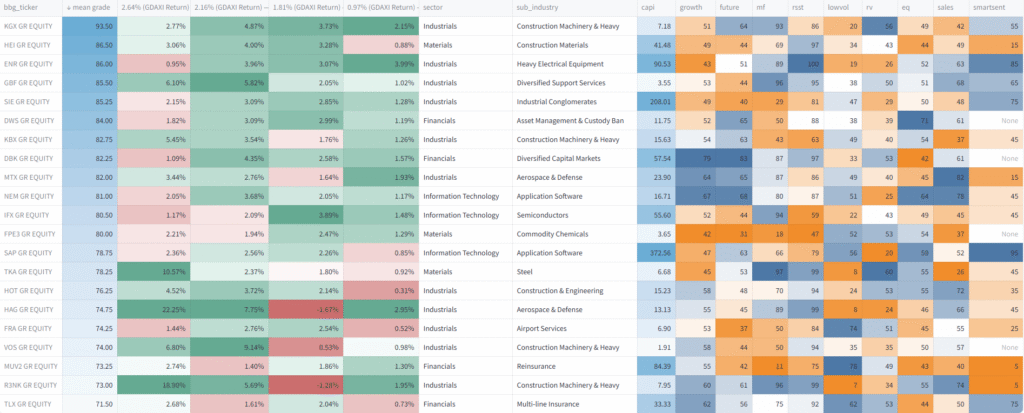

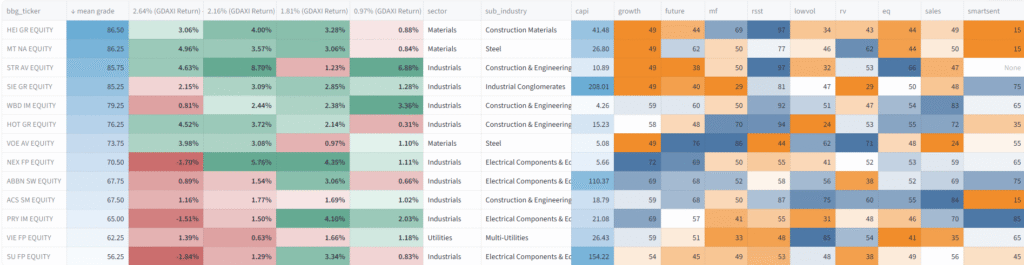

We now proceed to construct our portfolio. Each company is ranked on a scale from 0 (worst) to 100 (best), and the averages across the selected dates are computed to highlight those that demonstrate consistent outperformance. Afterward, we analyze the reasons behind their performance during these specific events. Since this fractal is named Der Kaiser, we only pick German stocks for the main basket. First, we present the selection and performance results, and then we move on to more detailed explanations and the definition of sub-baskets (where we also include non-German stocks).

For the sub-baskets, they are first defined by sector: for materials and energy these are relatively small baskets. Then, for industrials, we have one main basket that focuses only on industrials, which is a subset of our German-only portfolio. Since industrials are at the heart of this fractal, and given that Europe is expected to join the mix with a target of 2.1% growth in 2026, we also create thematic baskets within industrials: one for transportation and supply chain (industrial enablers), one for autos and auto-related services, one for small caps, since part of the funds will go directly to the Länder and finally one for Ukraine Peace. We assume that the stocks which performed well on those dates and are included in the Der Kaiser fractal will be the first to benefit from the reconstruction of Ukraine.

Energy

- Geopolitical & Economical Context

This sector is expected to be the primary beneficiary of the fiscal stimulus. Historically, the German economy has been built on industrial quality (“Deutsche Qualität”) and cheap Russian gas. The central question now is: who will replace that energy supplier?

Recent developments offer a potential answer. Following the update from the July 25-28 negotiations, a deal was struck between the EU, led by Commission President Ursula von der Leyen, and the U.S. This agreement stipulates a new 15% tariff on most EU goods exported to the U.S. However, a significant caveat remains: steel and aluminum will still be subject to a 50% tariff.

A key component of this accord is a pledge by the EU to purchase $750 billion in energy from the U.S. over three years, consisting mainly of LNG and oil. President Trump has explicitly stated that if the EU fails to meet the annual purchase target of $250 billion, tariffs will revert to 35%.

- Result

Our focus is on European grid operators and energy distributors, the companies responsible for moving and delivering energy across the continent. This also includes refineries on the coast. The sector is industrial, but these companies focus mainly on energy and electricity. Our target also includes companies that transform gas for construction, not just liquefied natural gas (LNG), such as Linde or Air Liquide.

- Siemens Energy AG (ENR): As a major provider of energy infrastructure, Siemens Energy could benefit from the increased gas imports from the U.S. and the broader push for grid modernization and energy security.

- Nordex SE (NDX1): A key player in wind turbine manufacturing, Nordex can capitalize on both infrastructure and climate transition spending. The stock’s potential is tied to the demand for cheap and reliable energy in Germany, where electricity prices for industrial consumers are nearly double those in France (Swiss Quote). A key risk to monitor is its sensitivity to copper prices, a critical component in its multi-megawatt turbines.

- Basket Energy : ENR, NDX1, LIN

Materials

- Geopolitical & Economical context

- The materials sector is key for Germany to reconstruct new housing or roads and to have a greener society. A part of the budget for climate and infrastructure will be construction.

- Added to that, with the meeting between the US and Russia on 15 August, groundwork was laid for a possible peace in Ukraine. So the big materials companies with high market cap have the ability to tackle such a challenge to reconstruct Ukraine. They need both cement and steel for construction. Materials also include chemicals that could benefit from tax breaks with the fiscal stimulus regarding research, but on a longer timeframe.

- On the other hand, regarding housing construction in Germany, we can also see some beneficiaries in the MDAX. This sector is fundamental to infrastructure development, but it faces specific headwinds. These small cap stocks could also benefit the allocation to the Länder.

- Result

- ThyssenKrupp AG (TKA): ThyssenKrupp, a major steel and industrial conglomerate, recently faced significant headwinds from the new EU-U.S. trade agreement, which imposed a 50% tariff on steel and aluminum. The U.S. market accounted for €6.08 billion of its €33 billion in revenue in 2024. While this represents a short-term loss, the company is a prime candidate to benefit from the domestic fiscal stimulus on a 1-year horizon due to the infrastructure push.

- Heidelberg Materials AG (HEI): A leading producer of construction materials like cement and asphalt, Heidelberg Materials is a direct beneficiary of infrastructure spending. However, a significant portion of its revenue comes from the U.S. (€4.43 billion out of €22 billion in 2024), making it susceptible to external market shifts. Invests in ‘decarbonated cement’ that can be sold 3x higher.

- LANXESS AG (LXS): This specialty chemicals company shows strong fundamentals with a Growth Grade of 30 and a Future Grade of 38. LANXESS can benefit from government tax breaks for research and development (R&D), providing key materials for both industrial and consumer applications. (Convexity title very low)

- Fuchs SE (FPE3): Engages in the development, production, and sale of lubricants and related specialties. Its products include engine oils, motorcycle lubricants, service fluids, greases, corrosion preventives, cleaners, and concrete release agents. The company also provides analytical, technical, open-gear, and coating services.

- Basket:

- Main driver: TKA, HEI, SZG, FPE3

- Convexity: BAS, WCH, LXS chemicals (Convexity, 1-year view, i.e., the time it takes for the company’s research to translate into buying new machines and putting them to use)

Industrials

- Geopolitical and Economic context

- This sector is at the heart of the fiscal stimulus and the fractal Der Kaiser. There are multiple declinations for this sector and different baskets possible. For this basket we do not focus only on Germany but take a broader view by including all European stocks. The first is the winner basket, with stocks already near ATH — they are the immediate winners from this plan. HEART

- We also have the enablers of industry and participants: all transportation will increase with this fiscal stimulus, as well as construction for those modes of transportation — mainly road and rail, but also airports (though less directly impacted by this fractal). ENABLER

- On the date of the Spring European forecast we saw many auto stocks surge, especially on that day. Auto construction is at the heart of the German economy, and the sector has been in free fall for 3 years. This plan will not let down such a huge part of the economy, which contains a large number of jobs. We can therefore be positioned early with convexity. AUTO

- Another angle for this fractal is small caps: at least €100 billion will be given back to the Länder and small caps, as Julius Baer explained in this article. We therefore also have a basket of small caps with very low Growth Grades but extremely low valuations. SMALL CAP

- German industrial giants are well positioned to spearhead the reconstruction efforts. We focus on specialized firms in civil engineering and heavy machinery, which are essential for rebuilding roads, bridges, and infrastructure from the ground up. Furthermore, the basket could include companies specializing in advanced building materials and electrical grid components, capturing the opportunity to not only rebuild, but also modernize Ukraine’s residential and commercial landscape with sustainable solutions.

- HEART

- Kion Group (KGX): KION Group AG engages in the sale and distribution of industrial trucks and the provision of supply chain solutions. (selling puts)

- Bilfinger SE (GBF): As a leading industrial services provider, Bilfinger is well-positioned to benefit from infrastructure spending. Its high Growth Grade (53) and Future Grade (44) indicate both strong current performance and solid future potential.

- Vossloh AG (VOS): Specializing in rail infrastructure and services, Vossloh is a direct play on the railway renovation component of the stimulus. With nearly 37% of long-distance trains delayed by more than six minutes, the need for investment in this sector is evident.

- Knorr-Bremse (KBX): A global leader in the manufacture and sale of braking systems for rail and commercial vehicles. Positioned across the entire supply chain, the stock is trading just below pre-tariff levels and has not yet broken out.

- MTU Aero Engines AG (MTX): A leading manufacturer of commercial and military engines, placing it at the top of the industrial value chain. (selling puts).

- Defence names: We also include our usual suspects in the defence sector, notably Renk Group (R3NK) and Hensoldt AG (HAG).

Enabler

- Kion Group (KGX): Kion is a major provider of industrial trucks, warehouse equipment, and supply chain solutions. Increased infrastructure investment will lead to greater logistical demands, making Kion’s products and services essential for efficient material handling and supply chain management. Solid play on the growing demand for intralogistics.

- Webuild S.p.A. (WBD): As one of Italy’s largest construction and civil engineering firms, Webuild is a major global player in large-scale infrastructure projects. The company’s expertise in building complex projects—such as railways, dams, and major civil works.

- KSB SE & Co. KGaA (KSB): A manufacturer of pumps and valves essential for power plants, water management, and industrial processes. KSB’s products are critical components for the infrastructure upgrades and industrial expansion targeted by the stimulus.

- Krones AG (KRN): A key player in industrial packaging, particularly for the beverage and food industries. As a stronger economy increases consumer activity and production, Krones will see a rise in demand for its packaging and bottling solutions.

- Jungheinrich AG (JUN3): Similar to Kion, Jungheinrich is a strong player in the warehouse equipment and material handling sector. It is poised to benefit from the increasing need for efficient intralogistics to support the economy’s renewed activity.

UKRAINE PEACE

- Heidelberg Materials AG (HEI): A global leader in cement, aggregates, and concrete, major player for rebuilding effort. The company previously had operations in Ukraine and would be essential for providing the core building materials needed for massive reconstruction projects.

- ArcelorMittal (MT): As one of the world’s largest steel manufacturers, ArcelorMittal is a critical supplier of raw materials. The company already has a major presence in Ukraine with its Kryvyi Rih plant.

- Strabag SE (STR): A major european construction company with a long history of infrastructure projects across Central and Eastern Europe. Strabag’s experience in large-scale civil engineering, road building, and civil works makes it a direct beneficiary of reconstruction contracts.

- Voestalpine AG (VOE): An Austrian-based steel and technology group with a focus on high-quality steel products. Voestalpine is well-suited to supply specialized steel for rebuilding railways, industrial plants, and other critical infrastructure.

- Nexans SA (NEX): Leader in advanced cabling and connectivity solutions. Rebuilding Ukraine’s power grid, telecommunications network, and transportation infrastructure will require extensive cabling, making Nexans a key enabler.

- ABB Ltd (ABBN): This technology group provides essential electrification and automation products and services. ABB’s expertise in power grids, industrial automation, and robotics will be vital for modernizing Ukraine’s energy and manufacturing sectors.

- Prysmian S.p.A. (PRY): The world leader in the energy and telecom cable systems industry. Prysmian’s role in rebuilding and expanding Ukraine’s power and data networks would be significant, making it a crucial infrastructure play.

- ACS, Actividades de Construcción y Servicios, S.A. (ACS): A Spanish construction and services company with extensive experience in large-scale infrastructure and industrial projects globally. Its expertise in managing complex civil engineering projects would make it a strong candidate for major reconstruction contracts.

- Schneider Electrics (SU): Because it’s French.

SMALL CAP

- Stabilus SE (STM): Specialized in motion control solutions, providing essential components like gas springs and dampers to the automotive, industrial machinery, and construction sectors. Its products are widely used in commercial vehicles and heavy equipment, positioning Stabilus to be a key enabler for the infrastructure and industrial projects fueled by the stimulus.

- Dürr AG (DUE): A mechanical and plant engineering firm that specializes in systems for the automotive and general industry. It is a key player in the clean technology sector, providing solutions for exhaust air purification and energy efficiency, making it an ideal investment for climate-focused initiatives.

- Norma Group SE (NOEJ): Specialized in engineered joining technology and fluid-handling systems. While not a direct builder of infrastructure, Norma Group’s products—such as clamps, connectors, and fluid systems—are essential components for a wide range of industries, including automotive, construction, and water management. The company’s technology is also used in modern cooling systems for electric vehicles and in water-saving applications, positioning it as a key enabler for both the infrastructure and climate-related goals of the stimulus.

- INDUS Holding AG (INH): A holding company specializing in the acquisition and development of small and medium-sized German industrial firms. This stock offers broad exposure to the German “Mittelstand,” which is a key target of the stimulus, providing diversified access to various industrial sectors poised for growth.

- Heidelberger Druckmaschinen AG (HDD): A leading global manufacturer of printing presses and other machinery for the print media industry. While not directly involved in construction, the company is a core part of the industrial machinery sector. In a significant new development, the company has entered the defense market through a strategic partnership with VINCORION to develop and industrialize power control systems, a new revenue stream that leverages its core industrial expertise.

AUTO

- Knorr-Bremse AG (KBX): Supplier of braking systems and other safety components for both trucks and rail vehicles, Knorr-Bremse is an indirect, yet critical, play on the fiscal stimulus. The increased demand for new commercial vehicles and trains, fueled by infrastructure and logistics projects, will drive revenue for Knorr-Bremse.

- Traton SE (8TRA): A global manufacturer of commercial vehicles under brands like MAN and Scania. Traton will be a direct beneficiary of the stimulus, as large-scale construction and transport projects will require a substantial number of new trucks and other commercial vehicles.

- Daimler Truck Holding AG (DTG): Large commercial vehicle manufacturers, Daimler Truck produces the heavy-duty vehicles and buses that are essential for major infrastructure projects. Its strong position makes it a prime candidate to capitalize on the increased demand for commercial vehicles generated by the German fiscal stimulus.

- Iveco Group (IVG): As a significant manufacturer of trucks and commercial vehicles, Iveco Group will benefit from the increased demand for logistics and construction transport fueled by the stimulus.

- AUTO1 Group SE (AG1): This German digital platform for used cars plays a distinct role in the automotive sector. While it doesn’t build vehicles, its success is tied to consumer confidence and overall economic activity, which a successful stimulus can boost. Moreover, the company is a key player in the electric vehicle (EV) market. Given the high purchase price of new EVs, the used-car market is becoming a crucial entry point for consumers. The platform’s business model, which includes both B2B and B2C channels, helps create more liquidity in the EV market by allowing businesses to efficiently resell low-mileage EVs to consumers at more accessible prices. This makes EV ownership more affordable and supports the broader transition to clean energy, aligning with the stimulus’s climate goals.